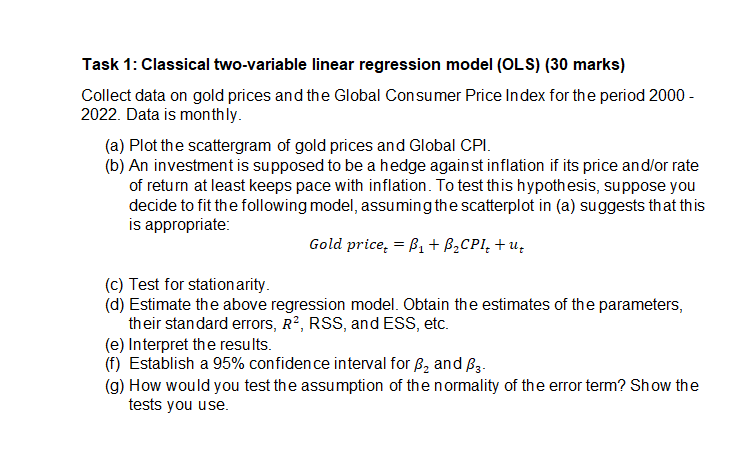

Task 1: Classical two-variable linear regression model (OLS) (30 marks)

Collect data on gold prices and the Global Consumer Price Index for the period 2000 -

2022. Data is monthly.

(a) Plot the scattergram of gold prices and Global CPI.

(b) An investment is supposed to be a hedge against inflation if its price and/or rate

of return at least keeps pace with inflation. To test this hypothesis, suppose you

decide to fit the following model, assuming the scatterplot in (a) suggests that this

is appropriate:

Gold price, =B₁ + B₂CPI₂+U₂

(c) Test for station arity.

(d) Estimate the above regression model. Obtain the estimates of the parameters,

their standard errors, R², RSS, and ESS, etc.

(e) Interpret the results.

(f) Establish a 95% confidence interval for ₂ and 33.

(g) How would you test the assumption of the normality of the error term? Show the

tests you use.

Fig: 1

Fig: 2